Great Advice, but wrong explanation!

“The end justifies the means” is not always good advice. The “Terminology Tip” in a recent Real Estate publication is a case in point. The Tip is a great idea but the explanation is wrong. On the basis of that great tip, one might be tempted to take further, more complicated mortgage advice from this non qualified Tipster.

First of all Real Estate Brokers are Real Estate Brokers. I would never advise anyone to sell their home without the services of a Real Estate Broker. A Real Estate Broker is well worth their fees many times over because there are many many litigious pitfalls for a novice DIYer to fall into and its your biggest investment of your life being put in jeopardy (for most people) if you make a mistake. Having said that, I would never advise anyone to acquire a mortgage without the services of a Mortgage Broker (use a Bank’s loan officer as a last resort because they have a biased, vested interest in your mortgage).

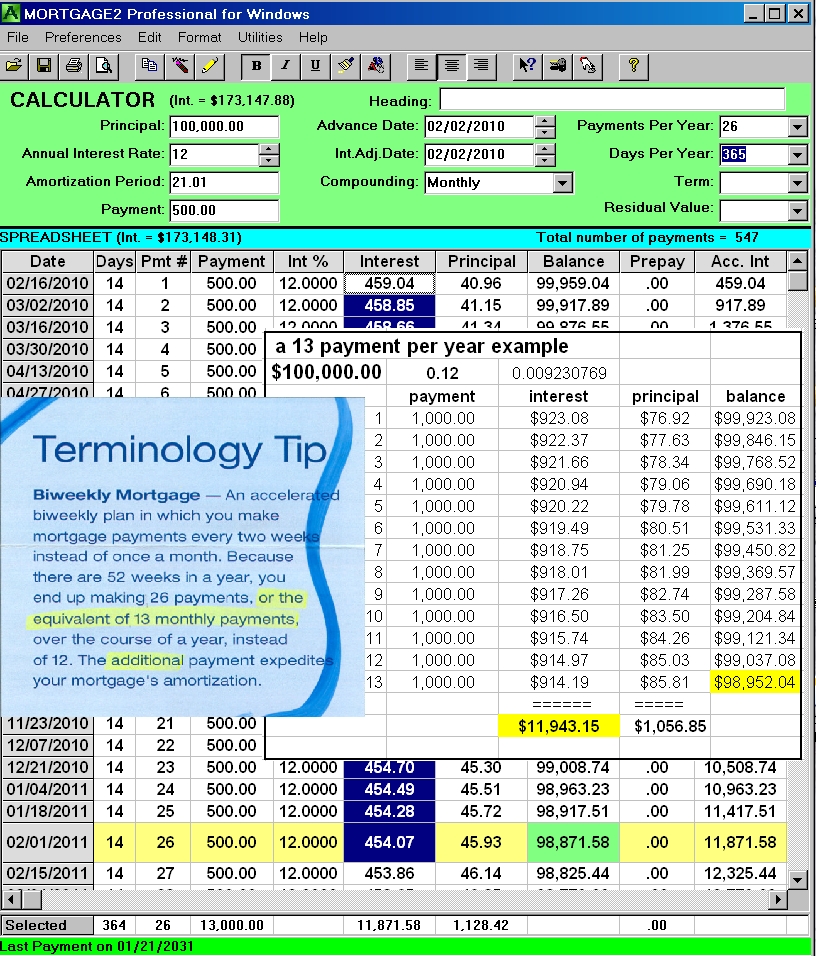

The biweekly mortgage is correctly touted as a great idea, which it is. The lowering of the amortization period (therefore minimizing interest costs) is because of the increase in the payment frequency NOT the equivalent of a 13 monthly payment plan as can easily be seen by the attached image example. The first year alone the biweekly plan costs $11,871 in interest vs $11,943 for the 13 payment per year plan! The longer one waits to make a payment the larger the interest accruing!

The “monthly compounding” method and 12 % as the annual interest rate were purposely chosen because it is easier to see the result of the interest factor by dividing 12 by 13. The same cash flow on a yearly basis was chosen ($13,000/year) in order to make the comparison.