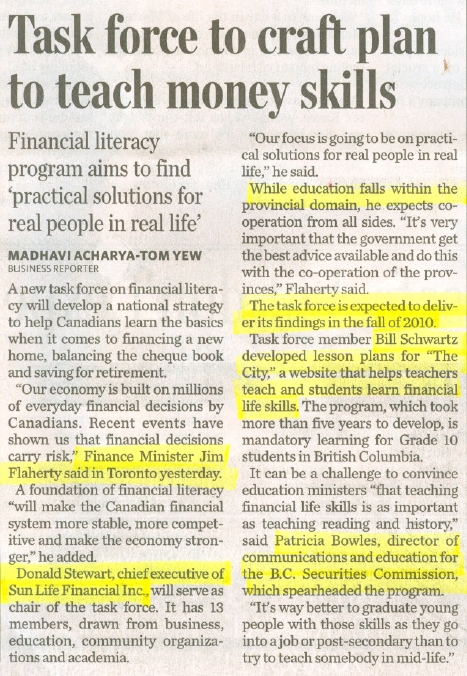

It was reported the three areas of concern are as follows;

Financing a home

Balancing the cheque book

Saving for retirement

Donald Stewart, CEO of Sun Life Financial, chairman of this new task force, said

“our focus is going to be on practical solutions for real people in real life”. Balancing a cheque book is practical and its common sense because most Canadians can do simple addition and subtraction!

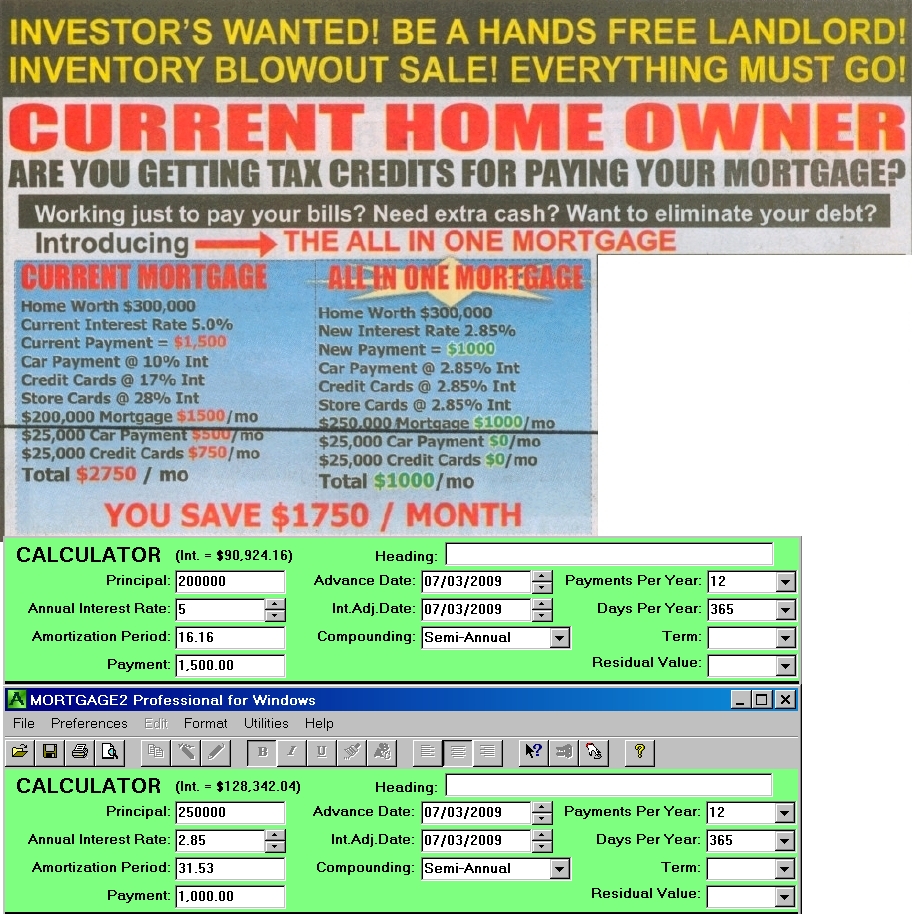

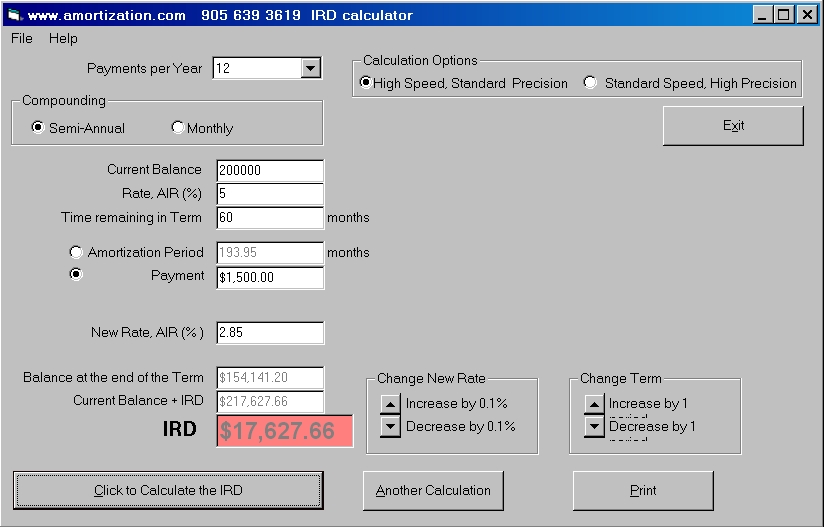

Saving for retirement is obviously practical and extremely important, however my concern is “Financing a home”. This task force is expected to deliver its findings in the fall of 2010. I assume this task force will addresses very important practical issues such as understanding mortgage interest calculations, compound interest, effective interest rates, cost of borrowing for a mortgage and premature mortgage renewal “penalties” such as Interest Rate Differentials (IRD).

A compulsory course, such as “Home Finance”, taught in Canadian high schools would be a very practical solution and prepare future Canadians for the real world. Hopefully, these new, “practical solutions for real people” will help Canadians understand advertisements such as the one that appeared in a current Canadian Real Estate publication. Lowering your monthly debt payments is realistic and a practical solution during these tough financial times. Canadians want to remain financially afloat and not lose their homes by defaulting on mortgage payments. However Canadians should also be aware of all costs of borrowing involved or be able to calculate them.