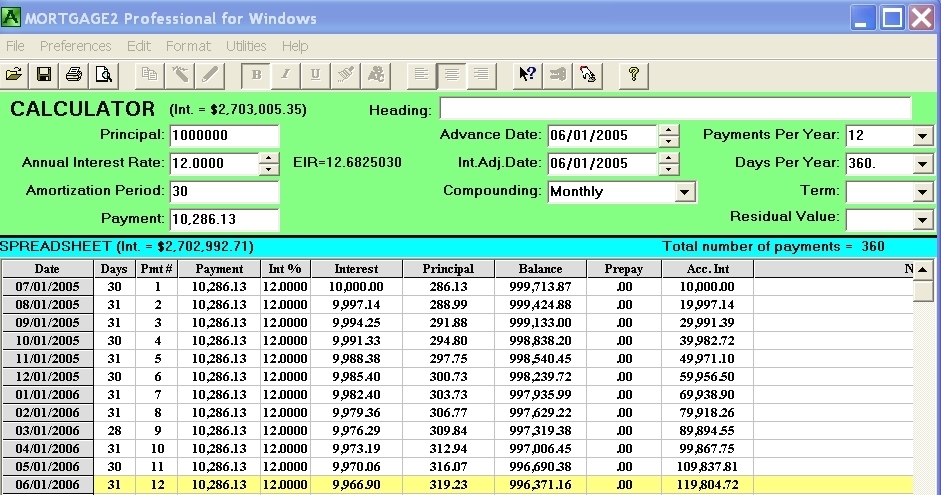

999,713.87 x (31/360) x .12 = 10,330.38

which is greater than the normal value of $9,997.14.

The prorating factor of 31/360 is because of the 31 day month. Financial calculators because of the algebra imply the year has 12 months with 30.416666 days per month (365/12=30.416666). The algebra basically divides the year into twelve equal parts. If one wanted to be real exact then the number 360 in the prorating factor should be 365 or better still 365.25

You can decide which interest calculation method you would rather pay, by comparing the following interest paid after one year.

Regular 360 Bankers year $119,805

Algebraic 365 exact day $119,817

360 prorate exact day $121,577

365 prorate exact day $119,970

365.25 prorate exact day $119,890

After one year it is obvious the 360 pro rated method give the lender the most interest out of the 5 methods outlined.

The disadvantage of the 3 prorated exact day methods is the cost of borrowing legislation in Canada and the USA will not make you aware of this situation if you don’t have an amortization schedule.