“I’m from Missouri. Show me.” is a state slogan and a wise expression. It analogous to accepting a scientist’s experimental conclusions at face value without checking the experimental data. My late Father, Alex Cirotto wisely taught me not to buy into anything unless I understood the concept and could verify any calculations. I am forever indebted to him.

As well as Banks, Credit card companies can be masters of “smoke and mirrors”. If you don’t understand the mathematics it can cost you big time. Misinformation is everywhere! Misinformation is everywhere even in print. Both Ellen Roseman in her article in the Toronto Star (“How to manage credit without credit managing you”, Aug 29 2010) and Patricia Levitt Reid in her National Post column (“Pay off your debt, don’t just pay it down”, July 24th 2010) confuses novices regarding compound interest.

Both of these advisors are perpetuating the myth that compound interest is the culprit working against you in borrowing. FACT: If your payment is one penny in excess of the interest due, YOU ARE NOT PAYING COMPOUND INTEREST. You are paying simple interest!

Compound interest is interest upon interest!

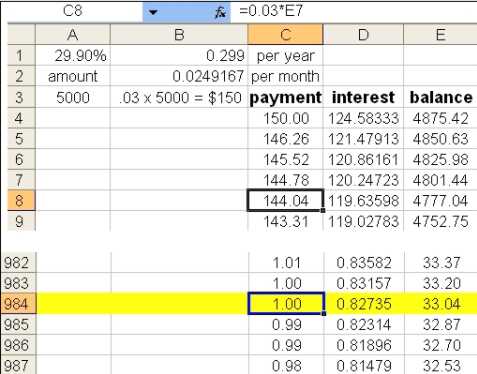

As you can see from the credit card example for an initial balance of $5000 at 29.9% per year, paying a minimum monthly payment of 3% of the outstanding balance takes a long long time to pay off a loan. You will also note that the payment is ALWAYS greater than the interest, thus NO COMPOUNDING! It takes almost 82 years to reach a point where the payment is one dollar per month and the balance is still $33.04.

Usually a credit card company will advise you that the monthly payment will be 3% of the current balance or $10 whichever is greater. The stated dollar value ($10) once reached, ends the agony sooner as the credit card company has already made most of their simple interest.