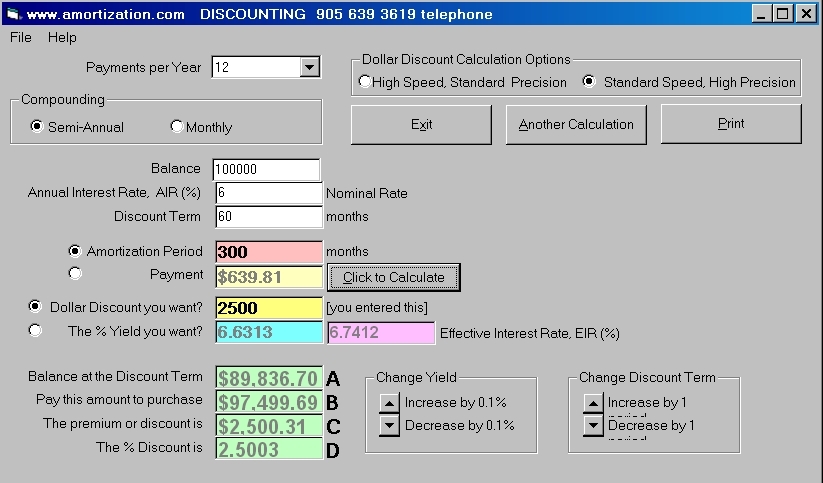

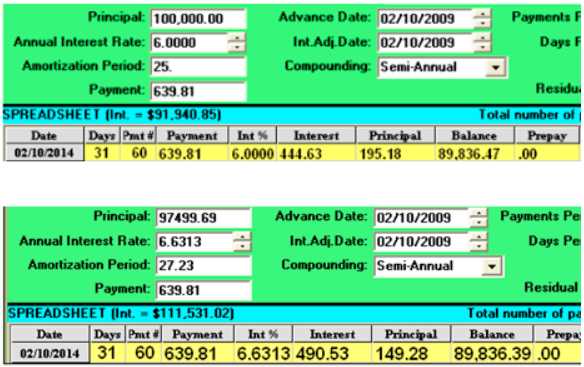

To do the cost of borrowing calculation, using the discount module, the total costs of $2500 is entered into the yellow input box, by first clicking on the radio dial, then clicking on the “Click to Calculate” button. To comply with the new Ontario legislation (January 1, 2009) the cost of borrowing is 6.6313%. In practical terms the cost of borrowing is 6.63% at two decimal places.

NOTE: Prior to January 1, 2009 the Ontario government would have required a mortgage broker, in this example, to quote the EIR of 6.7412% as the cost of borrowing.

The new legislation of January 1,2009 also specifies another new definition of APR. When I figure out how the new APR calculation is done I will post it on this web site.

To do a Discount calculation, again using the same discount module, the new lender might have said that he wanted a rate of 6.6313% if he bought your mortgage. The requested rate is entered into the blue input box by pressing the radio dial in front of “The % yield you want?” prompt.