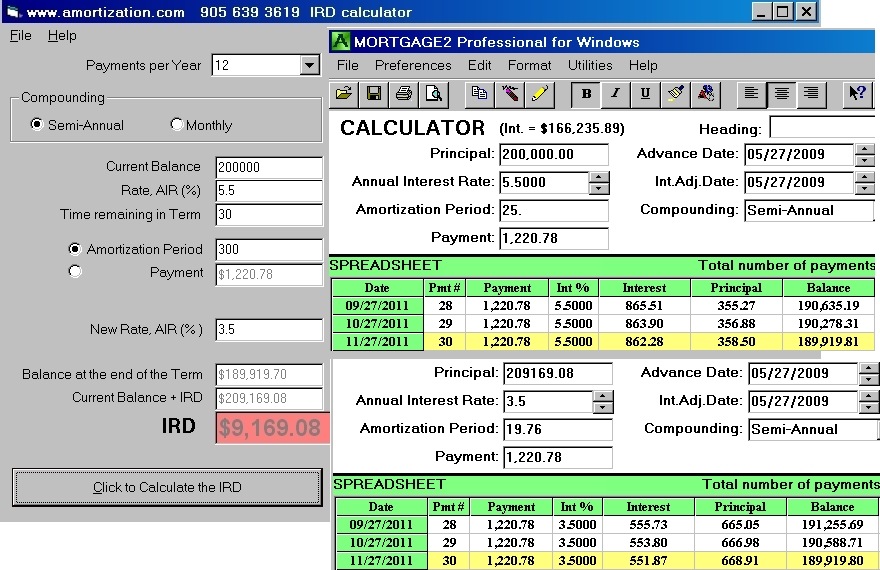

To use the newspaper example, the correct IRD should be $9,169.08 not the “about $12,000” as mentioned in the article. If the correct IRD is added to the $200,000 balance and the lower rate of 3.5% is used for the next 30 months (instead of the 5.5%) using the same monthly payments, the outstanding balance at the end of 30 months is the same (within 11 cents) which is what the IRD is intended to achieve. It is interesting to note that the IRD calculation is really nothing more than a mortgage discount calculation that virtually every registered professional mortgage broker knows how to perform!

An amortization period of 25 years was used as a basis in arriving at $9,169.08, however the $12,000 IRD from the Federal government’s web site is incorrect no matter what amortization period is chosen. If 35 years had been used the correct IRD would be $9,277 and if 15 years had been used the correct IRD would have been $8,884. The point I am trying to emphasize is Canadians should expect a standard method for calculating the IRD. If the Federal and/or Provincial governments are going to provide financial standards then they should get it right and be consistent on “help” websites and legislation! Anyone using that government calculator and its approximate numbers would be out by approximately $2831 which is a significant amount of money. An error of five or ten dollars, on a $200,000 mortgage I can live with but not $2831. Too many chefs spoil the broth, does come to mind!