Another reason I ask this APR question is because another area of confusion is the five major Banks have their own way of calculating an IRD early renewal “penalty” even though Canada Mortgage and Housing Corporation outlined a simple, logical method over 25 years ago that the Banks have ignored. Is this current APR calculation just more of the same old same old? In order to answer the APR question the following additional information must be stated in any advertising/calculation concerning a mortgage:

● Cost of borrowing charges (dollar value)

● Amortization period.

● The mortgage term.

● Payment frequency.

How does one calculate an APR when the interest rate could be changing each month?

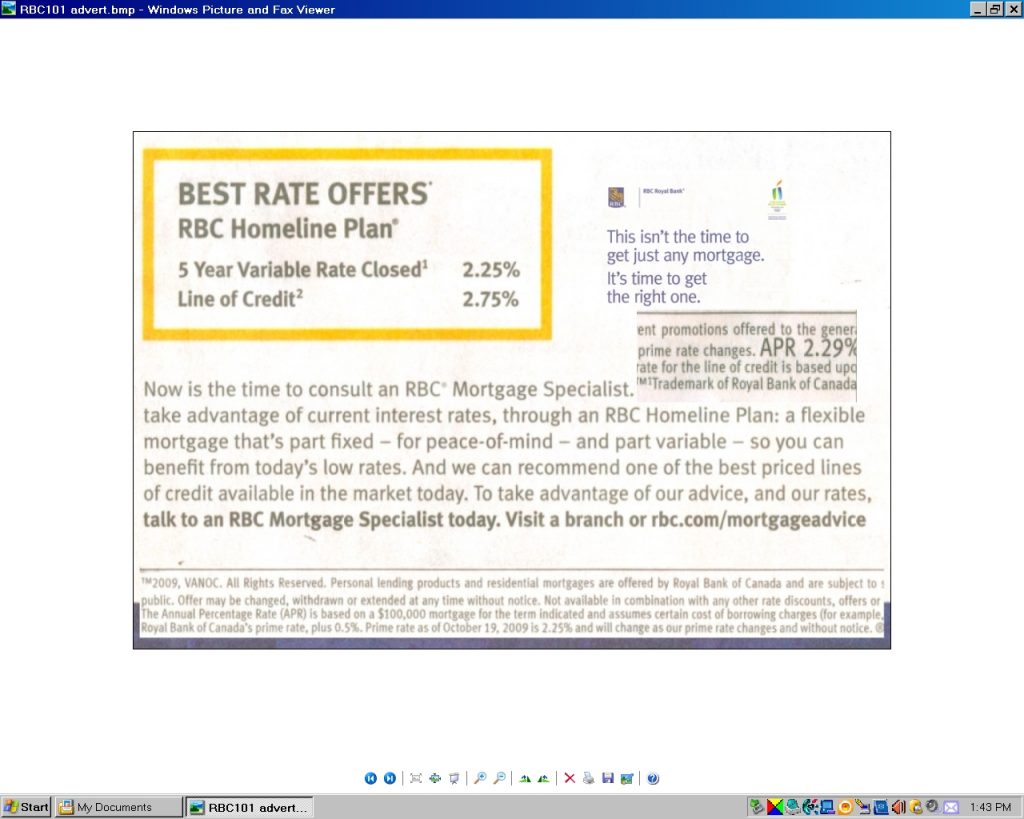

Is this APR in the RBC advertisement the same APR that the Ontario government mandated in 01/01/2009, that Ontario mortgage brokers must disclose?

SUGESTIONS:

●Use cost of borrowing fees of $1000.

●Use a 25 year amortization period.

●Use a monthly payment plan even though an accelerated weekly payment is better.

●Specify whether the APR calculation is based upon the term or the full amortization period as is required in the cost of borrowing calculation.

●Assume the interest rate is constant for the 5 year term at 2.25% (even though it’s a variable rate as in the RBC “example”).

●Specify if the mortgage is a traditional Canadian mortgage utilizing “semi annual compounding” or a non collateral mortgage utilizing “monthly compounding”.