A negative amortization schedule can be a positive experience

For the last 30 years I’ve continuously repeated my mantra at my seminars, …

“an amortization schedule, … don’t leave the bank without one”

because an amortization schedule is a financial roadmap showing you how to arrive at a debt free destination. Understanding an amortization schedule is the basis of ALL financial calculations. Fibonacci outlined this famous concept in his book in 1202 AD (“Liber Abacci”, Latin for, THE BOOK OF CALCULATIONS).

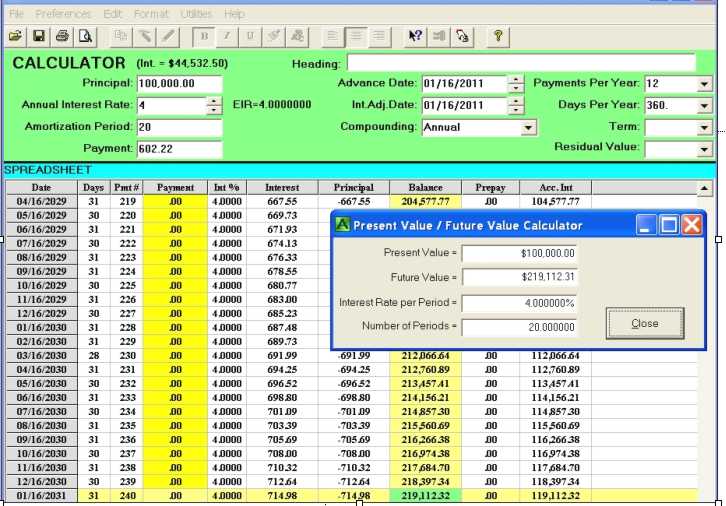

An online brokerage company’s advertisement in a National Canadian newspaper reminded me of another very important reason to have an amortization schedule, a negative amortization schedule to be precise! A negative amortization schedule is when payments are missed each month and the interest owing each month is added to the outstanding balance each month. In essence it’s a grid of future values of the initial Principal (present value).

This online brokerage company wants you to purchase your Mutual Funds through them because they will recoup some of the money you lose on your mutual funds due to management expense ratios (MER). The trailer fee (the money your financial planner gets every year whether your mutual fund grows or tanks) is imbedded in your MER. It is reinvested in your mutual fund giving you a better yearly return. This is an admirable and ethical product to consider, BUT, how good is it?

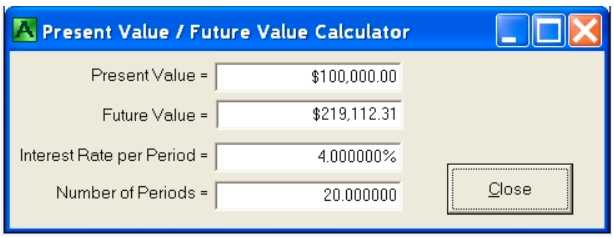

They use an example of $100,000 invested at 4% for 20 years.

Using any financial calculator you can perform a present value future value calculation to calculate the future value of $219,112 .